EY refere-se à organização global e pode se referir a uma ou mais das firmas-membro da Ernst & Young Global Limited, cada uma das quais é uma entidade legal separada. A Ernst & Young Global Limited, uma empresa britânica limitada por garantia, não presta serviços a clientes.

Artigos relacionados

Prepare-se agora para a nova era da globalização seletiva

Explorando cenários para o mundo em cinco anos revela caminhos divergentes para a geopolítica, políticas econômicas e estratégias empresariais. Saiba mais.

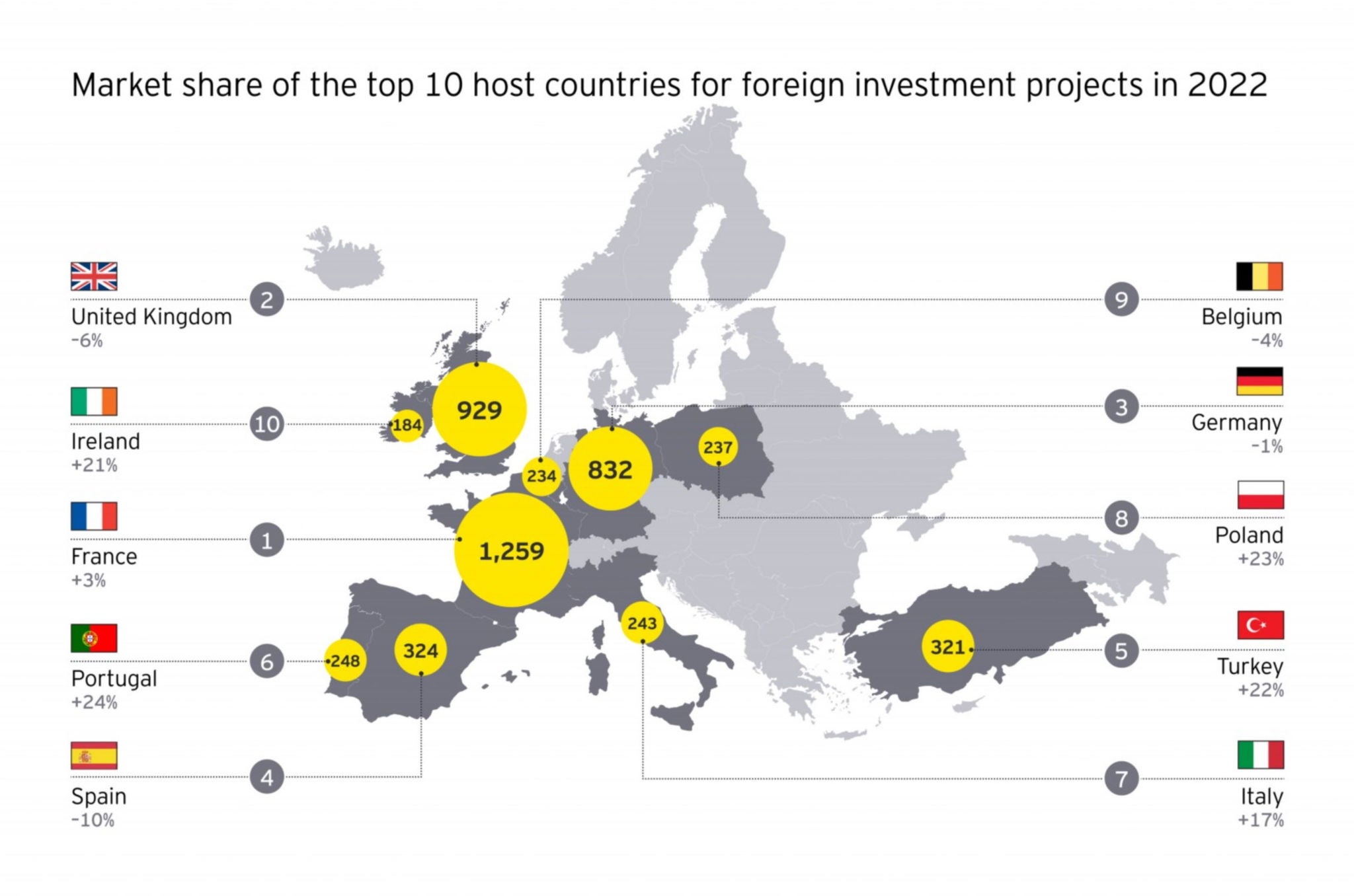

A pesquisa sugere que as empresas acham que o pior já passou. Um grande número de empresas pesquisadas — 67% — afirma ter planos de expandir ou estabelecer operações na Europa no próximo ano, um recorde histórico e acima dos 53% de um ano atrás. Isso reflete dois fatores que se cruzam: por um lado, a demanda reprimida e os planos diferidos dos últimos anos estão alimentando uma nova onda de investimentos em crescimento e capacidade; por outro lado, as condições econômicas exigem intensa atividade de reorganização, racionalização e otimização de custos.

Marc Lhermitte, Sócio, EY Consulting, Global Lead – FDI & Attractiveness, diz: “Se a Europa pretende capturar a demanda reprimida e os planos adiados, será essencial construir um caso de negócios atraente para investidores globais no contexto da concorrência dos EUA e da China”.

Os EUA estão atraindo investidores com sua Lei de Redução da Inflação (IRA). Para os estados membros da UE, o financiamento do programa de resiliência e recuperação da UE pode mudar substancialmente a evolução da economia da Europa. O programa foi projetado para oferecer um impulso econômico pós-pandemia por meio do suporte ao desenvolvimento digital, renovável e de habilidades.

“A ambição crítica da Europa deve ser criar as condições para as empresas fabricarem na Europa, investir em P&D e fazer os investimentos digitais e verdes que impulsionarão a prosperidade futura”, diz Julie Teigland, EY EMEIA Area Managing Partner. "A hora de agir é agora."