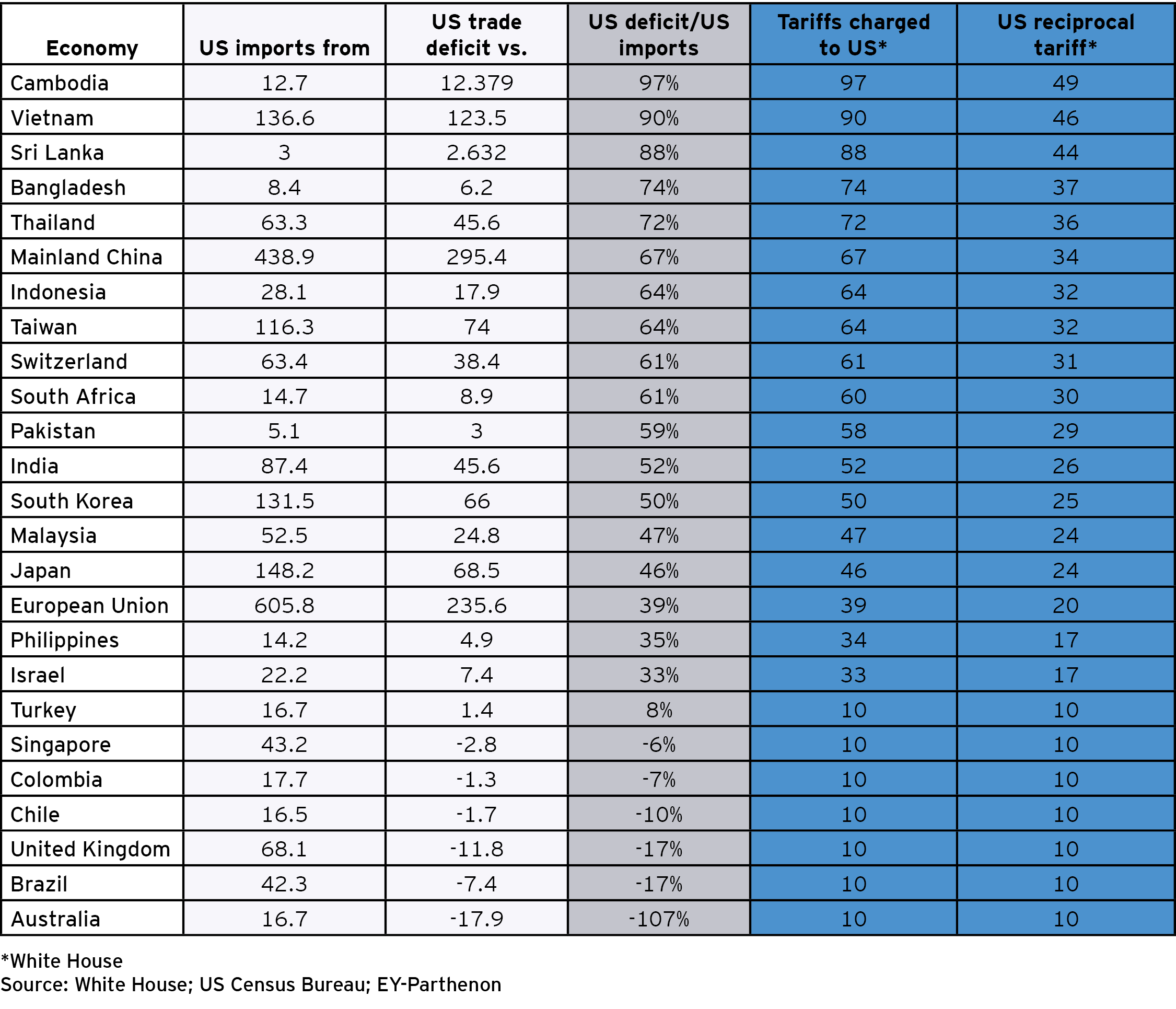

What other tariffs were announced?

The administration confirmed it is imposing automotive tariffs under Section 232 of the Trade Expansion Act (for which the original investigation concluded in February 2019), starting on April 3, citing national security concerns.

The 25% tariff affects imported passenger vehicles, including sedans, SUVs, crossovers, minivans and cargo vans, and light trucks. Key automobile parts such as engines, transmissions, powertrain parts and electrical components also fall under the tariff.

The US imported a total of US$247b of motor vehicles in 2024 plus US$143b of automotive parts. Assuming 90% of Canadian auto imports would eventually become USMCA-compliant and 95% of Mexican auto imports would become USMCA-compliant, that would represent a total of nearly US$300b of imports subject to the tariffs.

Assuming the tariffs are permanent, we estimate their impact to be a loss of 0.3% of GDP relative to a baseline in 2025, and a loss of 0.4% of GDP relative to a baseline in 2026. The impact on Consumer Price Index (CPI) inflation would +0.2% in 2025. For the EU, Canada and Mexico, the GDP loss relative to the baseline would be 0.1% in 2025 and 0.4% in 2026. For Japan, it would be 0.1% in 2025 and 0.3% in 2026. For mainland China, it would be 0.1% and 0.2% in 2025 and 2026, respectively.

What would the impact be of ending the ‘de minimis’ exemption for goods from mainland China and Hong Kong?

President Trump is ending duty-free de minimis treatment for covered goods from mainland China and Hong Kong. Starting May 2, these goods will be subject to a duty rate of either 30% of their value or US$25 per item (increasing to US$50 per item after June 1, 2025).

The de minimis tariff exemption allows shipments bound for US businesses and consumers valued under US$800 (per person, per day) to enter the US free of duty and taxes. In 2023, U.S. Customs and Border Protection estimated a total of over 1 billion such shipments worth around US$54b entered the US if shipped through the international postal network. Covered goods shipped from mainland China and Hong Kong are subject to the reciprocal duties and all other applicable duties.

While the total value of these shipments is modest compared to total US imports of over US$3t, research suggests that the elimination of the de minimis exemption would lead to a reduction in aggregate welfare around US$12b, disproportionately hurting lower-income consumers. Since roughly US$18b of de minimis shipments come from mainland China, mostly via e-commerce platforms, we estimate the loss of welfare from eliminating the mainland China exemption to represent around US$4b.

What will the impact be on our baseline forecast and what are the recession odds?

As described above, our initial assessment of the economic impact of the new tariff measures points to a substantial hit to the US and global economy, with consumer spending possibly retrenching and a risk that the economy could fall into a recession.

On the growth front, the US economy could enter a recession in the second half of the year with a real GDP growth drag averaging 0.8ppt in 2025, bringing our average growth forecast from 1.5% down to 0.7%. By Q4 2025, real GDP could be contracting 0.5% y/y.

On the inflation front, the new reciprocal tariffs could raise US consumer price inflation by 0.8ppt by Q4 2025, with the inflationary impulse concentrated in the second quarter of the year.

Given the uncertainty surrounding the duration of the new tariffs and potential retaliation measures from targeted economies, we will adjust our baseline in the coming week to account for the latest developments. One thing is for sure though, the likelihood of a recession in the next 12 months has risen from 40% just two weeks ago to around 60% today.

How will the Fed react?

Fed policymakers will maintain a reactionary stance in the coming month and will want to avoid front-running the impact of tariffs on output and inflation. We will likely see a growing fracture between those that are more concerned about the negative impact of tariffs on growth and employment and those more concerned about the risk of a de-anchoring of inflation expectations and persistently higher inflation.

How much certainty do we have about the permanence and breadth of these tariffs?

There will be latent uncertainty in the coming months surrounding the breadth of the tariffs and their duration. In terms of breadth, the administration has already started discussing the possibility of exemptions and exclusions at the country and sector levels. We will be producing a follow-up note with product-level analysis using the EY UPGRADE CGE model.

Similarly, we shouldn’t discount the possibility of some tariffs being imposed for a short period and then removed or reduced. Many economies have already begun to seek negotiations with the Trump administration to lower the tariffs.

On the flip side, it remains to be seen how the US administration will address certain products like pharmaceuticals, semiconductors, lumber, energy and critical minerals that were excluded from the recent tariff announcements but have been identified by President Trump as targets for future sectoral tariffs.

What is the risk for US consumers and businesses?

Beyond immediate cost pressures, higher tariffs will undermine corporate and household sentiment on the economy while diverting production resources to resilience building. With consumers and businesses increasingly worried about the economic outlook, a wait-and-see approach is likely to be favored, and both groups could scale back future spending and investment intentions. This is particularly true as trade uncertainty has fed market volatility, with the US equity market underperforming. The ensuing negative wealth effect is likely to further constrain business investment and consumer spending.

To offset both the challenges around trade uncertainty and the higher cost of doing trade, businesses will adjust their strategies. Some will diversify supply chains, shifting sourcing to economies less impacted by the tariffs, while others may invest in automation and cost take-out exercises to cut costs and reduce dependence on imports.

Beyond the short-term risks, what would the long-term (5- to 10-year) impact of reciprocal tariffs be?

We anticipate that the US economy will be among the economies most adversely affected by reciprocal tariffs, with the long-term impact on real GDP expected to be negative 0.7% — worth around US$200b annually.