EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

What are the key factors for stable semiconductor procurement?

In brief

- The global semiconductor market was approximately USD618 billion in 2022, and is projected to reach USD1 trillion by 2030.

- The semiconductor value chain is comprised of four stages: Design, manufacture, sale, and final products.

- Challenges within the semiconductor supply chain include imbalances between supply and demand, demand for custom specifications, the complexity of global supply chains, the regulation of materials, talent shortages, and the impact of tariffs and consumption tax.

- This article outlines effective approaches to mitigating semiconductor procurement issues and reconfiguring supply chains.

Semiconductors are one of a number of essential components that underpin modern society, as evident in their extensive presence in many of the products we depend on every day. Essential to the manufacture of computers, smartphones, automobiles and many other products, semiconductors make modern life possible.

However, the manufacturing of semiconductors requires both sophisticated technology and substantial investments, and is largely clustered in a select group of countries and companies. These factors generate a number of risks in semiconductor supply chains. COVID-19, US-China trade frictions, and other events of recent years have increased the severity of the global semiconductor shortage and impacted a wide swath of industries. One example of this impact is automobile manufacturers forced to delay production plans, despite increased demand for their products, due to component supply issues caused by the semiconductor shortage.

In light of such vulnerabilities, resiliency and diversity in the supply chain are now recognized as urgent and critical aspects of ensuring economic security and resolving other issues. One particularly notable risk is the current dependence on the cluster of countries and companies that produce semiconductors. These and other external factors pose challenges that companies can only surmount with sophisticated semiconductor sourcing strategies.

The semiconductor market in detail

Semiconductor Equipment and Materials International (SEMI) valued the 2022 global semiconductor market at approximately USD618 billion and projects that the market will reach USD1 trillion by 2030. While smartphones and computers remain the strongest source of demand for chips on the semiconductor market, increased use in other applications (e.g., in automobiles and IoT devices) has resulted in dramatic increases in overall demand for semiconductors in recent years. Demand for semiconductors is expected to increase further due to advancements in AI, blockchains and other new technologies.

The semiconductor value chain

- Design: This stage encompasses the design of semiconductor functions and performance. While some companies complete this process themselves, it is often performed by specialized companies known as design houses.

- Manufacture: This stage encompasses the manufacture of semiconductor raw materials and components, including wafers, masks, and packages. The manufacturing process can be further divided into the front-end and back-end processes. The front-end process is the process of forming circuits on the wafer, and this process is mainly handled by specialized companies called foundries. The back-end segment consists of wafer dicing, packaging, and testing, and is typically conducted by foundries or assembly and testing companies.

- Sale: This stage encompasses the offering of semiconductor products and services on the market by semiconductor manufacturers and trading companies.

- Final products: This stage encompasses the exploitation of semiconductor features for the design and manufacture of products and systems that serve a wide variety of purposes, such as computers, smartphones, and automobiles. Finished product manufacturers and EMS are in charge of final productization. These companies work closely with semiconductor suppliers and customers to provide the best products for market needs.

Challenges for semiconductor supply chains

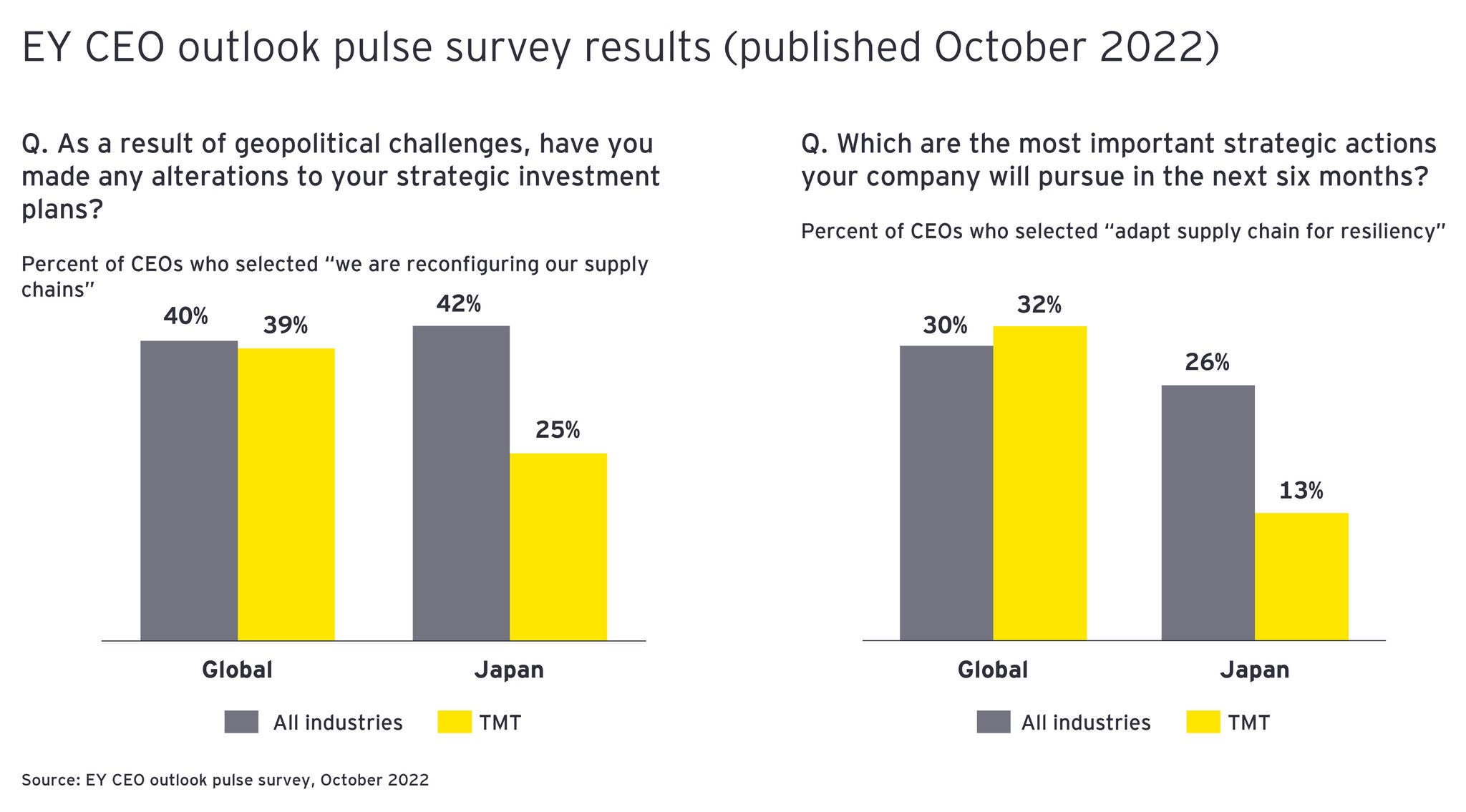

The EY CEO Outlook Pulse Survey shows that as many as 40% of CEOs responded that they have reconfigured their supply chains to address geopolitical challenges. In contrast with the global response, a mere 25% of CEOs in Japan's TMT industry responded that they have reconfigured their supply chains. Moreover, only 13% of CEOs in Japan's TMT industry responded that they aimed to adapt the supply chain for resiliency as part of their strategic initiatives in the next six months, marking another low figure compared to the 32% of global CEOs who responded similarly.

As evident from these survey responses, the challenges facing the supply chains in general are great in number. Below is a summary the challenges relevant to semiconductor procurement.

- Imbalances between supply and demand: While semiconductors are components required for a large range of products including smartphones, computers, and automobiles, COVID-19, natural disasters and other factors have caused production slowdowns and supply shortages. In the automobile industry, such events could result in delays in product delivery. According to SEMI Japan president Masahiko Hamajima, procurement of semiconductors has become an issue not only for automobile production but also in concern to the production of the medical devices necessary for ECMO and MRI, and is regarded a major issue by the Ministry of Economy, Trade and Industry. He also notes a compounding issue in that semiconductor manufacturers do not have many incentives to produce the semiconductors used in the medical sector, as they utilize older generations of technology, are purchased in comparatively low volumes and have notably high reliability requirements.

- Custom specifications: Semiconductors are designed to serve a variety of applications and functionality requirements, and thus exist as a diverse spectrum of products. This in turn generates additional complexity and costs for the manufacturing process and in inventory management. Additionally, companies must maintain a flexible and effective supply chain in order to stay agile and respond quickly to market fluctuations. This highlights the importance of striking a balance between high degrees of customization in procured semiconductor components and the optimization of the supply chain.

- Complexity of the global supply chain: Semiconductor manufacturing is enabled by a complex global network involving a large number of the world's countries and companies. This supply chain is comprised of multiple stages and actors, from the supply of raw materials, design, manufacturing and assembly/testing to sales. The large number of processes and international divisions of labor required in semiconductor manufacturing produce by necessity the complex, global nature of the semiconductor supply chain. Nippon Electronic Device Industry Association president Shozo Saito comments that outsourced semiconductor assembly and test (OSAT) companies responsible for the back-end segment of the manufacturing have particularly strong presences outside of Japan, adding that if materials are procured for the front-end segment to be conducted in Japan, the end-segment is conducted in another country, and the final testing is conducted in Japan, these repeated imports and exports extend lead times and preclude the ability of companies to make timely adjustments to market fluctuations.

Source: Created by EY based on SIA materials

*When playing the video, please maximize the screen size.

Transfer pricing taxation is also one of the major challenges for such semiconductor supply chains. The transfer pricing rules require appropriate prices for related party transactions and allocate taxation rights among the countries involved in the transaction. Transfer pricing rules are internationally aligned and, in principle, are based on the arm's length principle where related party transactions should be conducted under the same terms and conditions with independent third party transactions. However, there are many cases where it is practically difficult to apply the arm’s length principle into the semiconductor supply chain. For example, intellectual property regarding the design and development of semiconductors is not commonly transacted in the market, and therefore providing an objective evaluation of its value can be impracticable. The risks and functions related to the manufacturing and sale of semiconductors are not distributed equally among companies within the supply chain, and explicit identification of that distributions can be also challenging.

- Regulation of materials: New regulations affecting per- and poly-fluoroalkylated substances (PFAS) are being discussed in the US and Europe and could come into effect as early as 2025. SEMI Japan president Masahiko Hamajima stated that because PFAS are used in various stages of semiconductor manufacturing, and photoresists in particular are essential to the manufacturing of advanced semiconductors, forbidding their use could render manufacturing of such products impossible, and hence the transition to safe alternative materials is now a pressing issue for the industry. He also stated that developing PFAS-free alternative materials will take time, with some industry insiders predicting a timeframe of 15 years or longer for a complete transition.

- Talent shortage: Semiconductor manufacturing requires a high degree of skills and knowledge, and the industry is in need of talent with specialist capabilities. However, the rapid growth of the semiconductor industry in recent years has only exacerbated the talent shortage. The shortage of engineers and other workers with technical capabilities is particularly significant, a sign of the lack of workers with specialist knowledge of the production line design, controls and other aspects of the manufacturing process. Demand for semiconductors is surging, and each launch of a new manufacturing plant or R&D location can result in an additional crunch for talent. Talent shortages of this nature have a substantial impact on productivity and the quality of semiconductor products. Increases in the loss of industry talent and company attrition rates are also present issues that give additional weight to the importance of talent acquisition and training within the industry.

- Impact of tariffs and consumption tax incurred upon inventory adjustments and supply chain reconfigurations: The balance between demand and supply is a significant factor in the semiconductor market, where sudden fluctuations in demand cause inventory shortages, yet stagnations in demand result in excess inventory and the need to dispose of such inventory. For these reasons, manufacturers must swiftly implement targeted measures in response to market conditions, such as optimizing inventory management practices and expanding or shrinking production lines. Supply chain reconfigurations also result in tariffs and consumption tax implications. Semiconductor products are transacted on the global market, and reconfiguration of a supply chain necessitates the completion of numerous procedures pertaining to import/export, logistics, and other facets of such transactions. Additional tariffs and consumption tax could result in increased product prices, while import/export procedures could give rise to delivery delays.

Given this complex environment, what can procurers of semiconductors do to insulate themselves from supply chain risk?

Key facets of supply chain reconfiguration

Companies have begun adopting a different approach to semiconductor procurement, prompted by the prolonged shortage of semiconductors in recent years. The following are effective countermeasures that can be taken in response to the latest such developments.

Supplier diversification and centralized purchasing

- Supplier diversification can mitigate the risk of being dependent on a single source for procurement. Having multiple sources of supply facilitates consistency in procurement and enhances price competitiveness.

- Centralized purchasing streamlines the procurement process and lowers the effort required to conduct inventory management. For example, Toyota Motor Corporation has allied with DENSO Corporation and other Toyota Group companies to introduce centralized purchasing; the parties share information relevant to the product supply chain even as products undergo R&D, are accelerating the intercompatibility of semiconductor design and switching to the use of generic semiconductors. Such actions assist semiconductor manufacturers in production planning and bring increased productivity, which enables the Toyota Group to enhance their purchasing power through efficiencies of scale.

Achieving greater supply chain transparency and building collaborative relationships with semiconductor suppliers

- In order to achieve greater supply chain transparency, it is essential that companies collaborate and exchange information with semiconductor suppliers and trading companies.

- Other effective methods include building traceability or digitalization into the entire supply chain. These are challenges that cannot be addressed solely by the companies that procure semiconductors, and in fact require the building of collaborative relationships with semiconductor suppliers to address. Nippon Electronic Device Industry Association president Shozo Saito has shared his comments from this perspective, stating that it is important to approach solutions by creating a seamless supply chain by partnering with suppliers during design, development and later stages, and adding that companies must move beyond the concepts of supplier and purchaser and approach suppliers as business partners.

In light of this input, achieving consistent success in procurement amidst the constraint of lengthy lead times for semiconductors requires that companies give due consideration to aligning their purchasing order timelines for consistency with semiconductor production lead times. One-sided demands for a semiconductor supplier to address uncertainties arising from inconsistencies between semiconductor production lead time and the timing of purchasing orders could instead have an adverse effect on any business partner relationship that could be built with such a supplier. Another important method of achieving greater transparency and strengthening business partner relationships with suppliers is to share production, sales, and inventory data (PSI data) on a shared platform, and thereby use ordinary operations to address uncertainties.

Accurate demand forecasting and consideration of alternative solutions

- Product demand fluctuates depending on market trends and advancements in technology. Accurate forecasting is therefore a crucial prerequisite when concluding long-term contracts with semiconductor manufacturers to secure a consistent supply, as it enables the purchaser to secure a long-term contract for production capacity from such manufacturers.

- The use of alternative or generic products is also an effective way to address instability in semiconductor supply. These measures alleviate the impact of price surges and shortage of semiconductors. With that said, the use of alternative semiconductor products may require alterations to product designs or specifications, and it is important to prepare to accommodate such changes to product designs and specifications. In regard to mid-to-long term consistency of supply, SEMI Japan president Masahiko Hamajima commented that it is also important to use components that utilize the latest technology to the full extent possible, giving an example of automobiles to illustrate how impacts could be mitigated by using standardized components and 16nm to 28nm nodes rather than legacy nodes of class 40nm to 60nm, for which it can be difficult to guarantee long-term availability.

Adapting the semiconductor supply chain to the changing tax environment

- Numerous international transactions take place within the semiconductor supply chain, which means that it can easily be affected by changes in the taxation and tariff policies of any relevant country, and it is therefore important that companies manage taxation risks and formulate appropriate tax strategies. While transfer pricing presents a range of complex and challenging issues in the context of the semiconductor supply chain, taking the appropriate actions to address such challenges will also prove beneficial in the design of an effective supply chain.

【Authors】

Supply Chain and Operations

Kenji Hirai (Partner)

Ichiro Saito (Senior manager)

Ernst & Young Tax Co.

Takashi Ajita (Partner)

Technology, Media & Entertainment, and Telecommunications (TMT)

Kyoko Hasegawa (Consultant)

Tetsuo Kan (Consultant)

*Affiliations and titles are as of the time of the publication of this article.

Summary

The semiconductor industry provides infrastructure essential to any digital society, and its supply chains are made of complex webs that traverse multiple countries. Semiconductor supply chains are affected by a host of challenges including talent shortages and the regulation of materials. Such issues make reconfiguring the semiconductor procurement component of corporate supply chains a key facet in enhancing resilience in parts procurement for the greater manufacturing industry.