EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

Tax policy advisory services by EY India offers insights & strategies to navigate complex tax regulations, driving business growth and compliance.

Read more

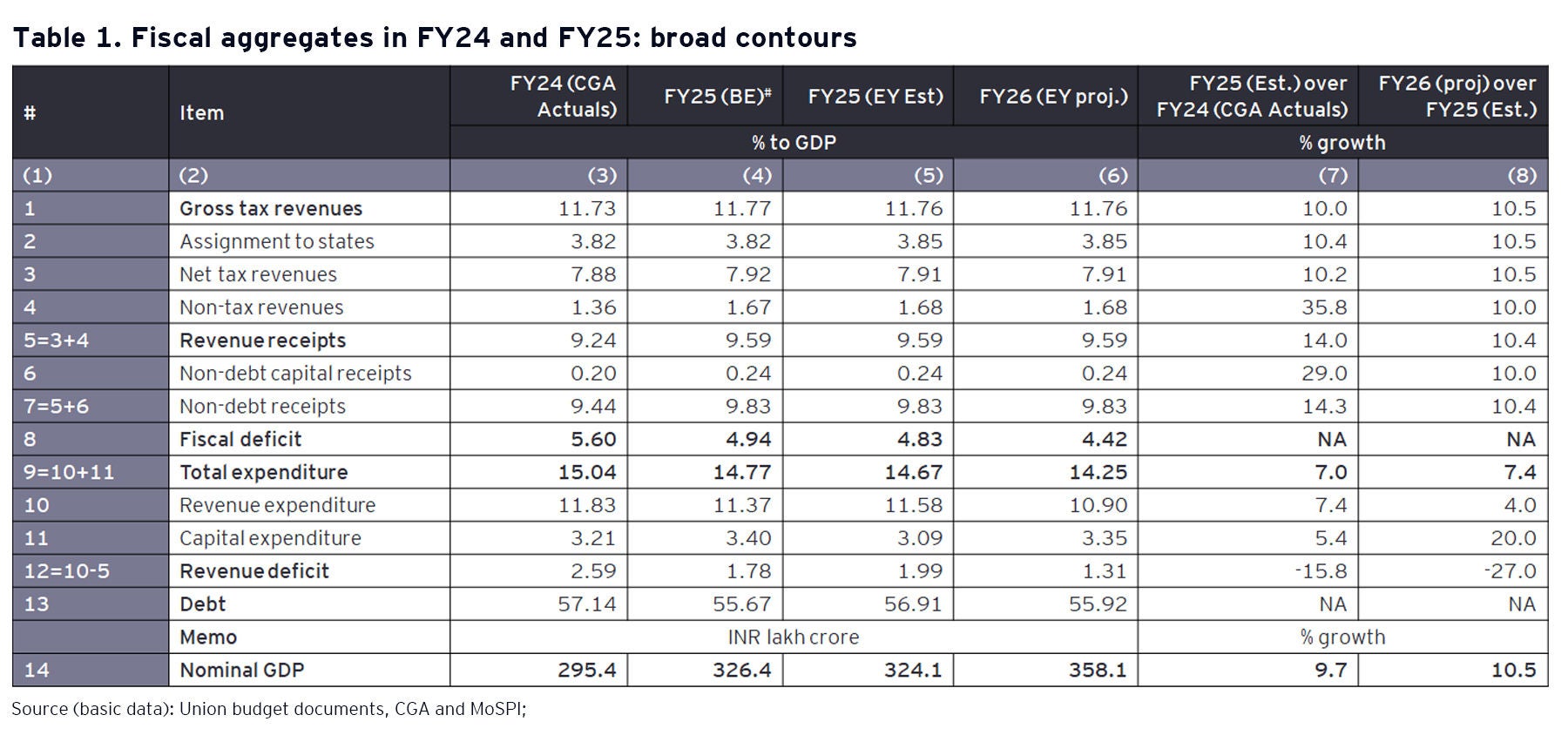

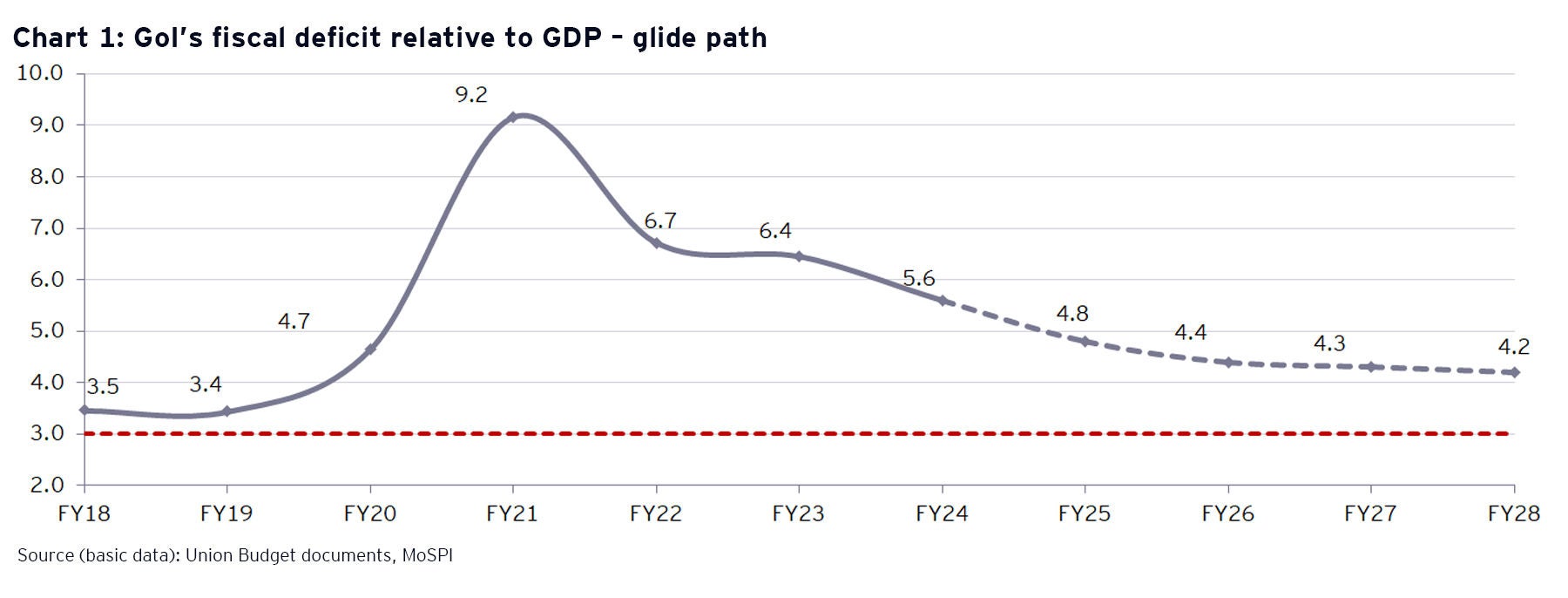

In FY26, the main fiscal policy intervention required would be an attempt to restore infrastructure expansion momentum to support real GDP growth. There would be some positive movement on fiscal consolidation both in FY25 and FY26. Some other changes in the FY26 budget may relate to the revision of import tariffs and some rationalization of personal income tax rate and its deduction structure.

In the medium-term, in view of the impact of Eighth Pay Commission recommendations, the path of fiscal consolidation would lose momentum. We consider that, in the medium-term, real GDP growth can still be maintained at 6.5% and nominal GDP growth at 10.5% with some inter-year variations. A combination of slower nominal GDP growth in FY24 and FY25 and pressure on the INR may push the US$5 trillion Indian economy milestone from FY28 to FY30. To address this, nominal GDP growth must recover to at least 10.5% beyond FY25, and INR depreciation against the US$ must be moderated.