EY refers to the global organisation, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

As climate-related transition plans become mandatory for many New Zealand businesses, companies are investigating cost-efficient ways to reduce their greenhouse gas (GHG) emissions.

Organisations considering the procurement of renewable energy using market-based instruments, such as Renewable Energy Certificates (RECs) within New Zealand need to be aware of the evolving domestic and international context for the use of these products. Used appropriately, these contracts can provide material financial support for decarbonisation efforts.

However, the high percentage of renewable electricity already available on New Zealand’s power market means that careful due diligence is needed about any climate-related claims made with the use of these products.

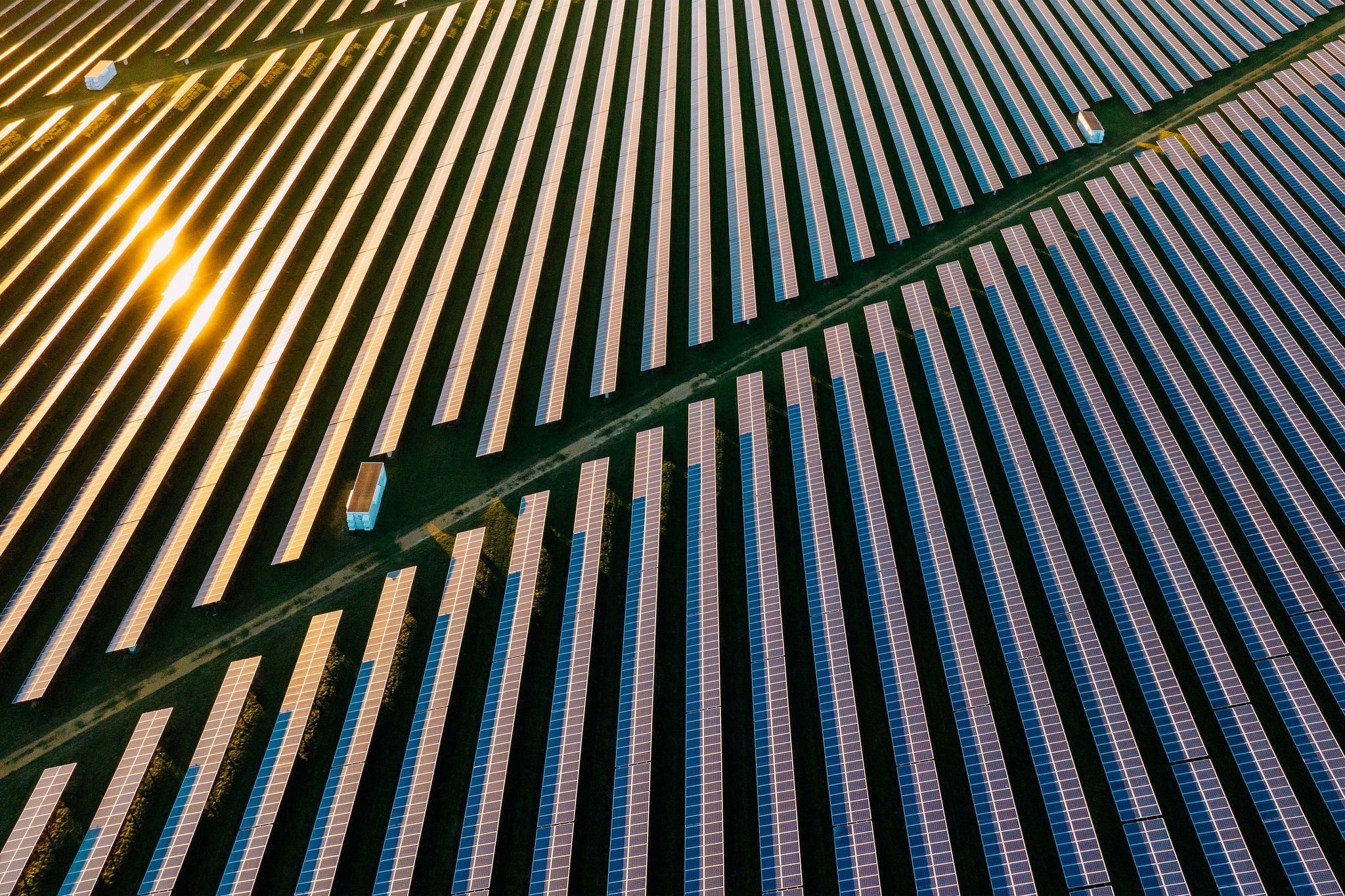

What is a REC? A Renewable Energy Certificate (REC) is a market-based instrument that represents the property rights to the environmental attributes of renewable electricity generation. One REC is typically equivalent to one megawatt-hour (MWh) of electricity generated from a renewable energy resource. When renewable energy is generated, it produces environmental benefits, such as the reduction of greenhouse gases and other pollutants compared to conventional fossil fuel-based electricity.

Download Renewable Energy Reporting: Challenges and opportunities in New Zealand

Summary

Organisations in New Zealand should exercise due diligence when considering Renewable Energy Certificates (RECs) as part of their transition plans to reduce GHG emissions, given the country's already high percentage of renewable power and the evolving international standards for REC usage.

EY can assist with strategic advice on decarbonisation, evaluating REC products, and assessing the suitability of renewable investments and Power Purchase Agreements (PPAs) in accordance with international reporting standards and additionality requirements.