EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Recent Searches

In the face of an unpredictable global economy, investors are seeking out resilient and profitable asset classes.

Forestry and timber funds are emerging as a sustainable and attractive asset for investors. With the growing awareness around climate change and the rising demand for timber products, this "green goldmine" is proving to be a promising avenue for long-term capital growth. Let's dive deep into the increasing interest in investing in timber and forestry and explore the benefits and risks of this alternative asset class.

Overview of the asset class

Forestry funds, also known as timber funds, are investment vehicles that provide exposure to the forestry industry. These funds typically invest in forested land or timber assets, such as lumber or pulp, and may also invest in timber-related companies. The goal of forestry funds is to generate returns for investors by harvesting and selling timber or other wood products.

There are various types of forestry funds available to investors, including open-end funds, closed-end funds, exchange-traded funds (ETFs). The structure of these funds can vary depending on the fund manager and their investment strategy. The fund manager will typically have a team of forestry experts who are responsible for managing the land and timber assets, as well as making investment decisions on behalf of the fund.

The management of forestry funds requires specialized expertise in forestry and land management, and fund managers may work closely with forestry experts to ensure the proper management and sustainable maintenance of the land and timber assets.

A look at the past decades

Historically, timberland was predominantly possessed by wealthy families, corporations, and governments. However, approximately 50 years ago, this practice started to change, resulting in a timberland investment climate that has evolved and adapted to suit changing market trends, environmental conditions and investor demands.

Following the implementation of the US Employee Retirement Income Security Act in 1974, pension funds started considering timberland to diversify their investments and minimize the risk of significant losses[1]. This increased demand for timberland in the 1980s coincided with the restructuring of the forest products industry in the US, leading to a shift in timberland ownership from operating companies to financial investors. To handle these transactions and oversee investment partnerships, Timber Investment Management Organizations (TIMOs) appeared.

Over the years, these investment strategies have produced strong and consistent returns through cash yield and capital appreciation. The globalization of the forest products sector, particularly the growing demand for fiber in Asia, has led to the development of timberland investment markets outside the US, such as in Latin America, Oceania and Europe.

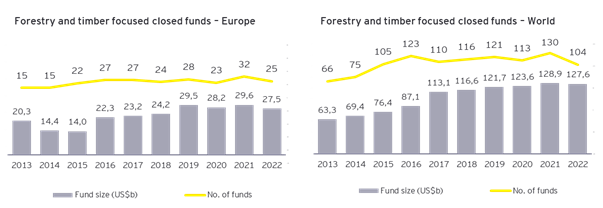

According to data from Pitchbook, the global number of closed forestry and timber funds has fluctuated over the past two decades, with a peak of 130 funds in 2021 and a low of just seven in 2003. In 2022 there were 104 closed funds globally with a focus on forestry and timber investments, with a median IRR of 15.45%. This is a slight decrease from the previous year's median IRR of 16.43%, but still represents a solid return for investors.

Looking back over the past decade, the data shows that the number of funds globally has remained relatively consistent, with some fluctuations year on year. However, the median IRRs[1] have consistently remained in the double digits, ranging from 10.06% in 2015 to a high of 16.43% in 2021. Even in years of economic turbulence, such as the global financial crisis in 2008, timber and forestry funds have demonstrated resilience and provided attractive returns for institutional investors.

“From trees to returns”: the benefits of investing in forestry funds

One of the primary benefits of investing in timber and forestry is the potential for long-term growth. Timber is a slow-growing asset, and it can take years or even decades for a tree to reach maturity. However, once a tree is harvested, it can be sold for lumber, pulp and other wood products, generating a return on investment. Additionally, the value of timberland tends to appreciate over time, and timber prices tend to increase as demand for wood products grows.

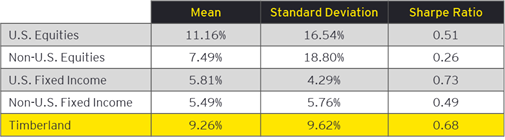

According to a report from Nuveen Natural Capital, forestry is an attractive investment due to its strong market fundamentals, stable cash yield, diversification benefits, hedge against inflation, and quantifiable climate benefits. The report also found that timber has outperformed many traditional asset classes since 1992, with an average return of 9.26% per year over the past 28 years:

28-year performance of timberland and traditional asset classes (Annual returns, 1992 – 2020)

In comparison, US fixed income had an average return of 5.81%, non-US fixed income had an average return of 5.49%, US equities had an average return of 11.16%, and non-US equities had an average return of 7.5%. Despite US equities performing better, they also had a higher level of volatility compared to timber.

Investing in timber and forestry can also have positive environmental impacts. Sustainable forest management practices can help reduce the impact of deforestation, promote biodiversity and protect ecosystems. Furthermore, trees absorb carbon dioxide from the atmosphere, helping to reduce greenhouse gas emissions and mitigate climate change. Most timber and forestry investment funds are focused on sustainable forestry practices and responsible land management. The areas of value creation within forestry assets have been crystalizing over the past years; examples of which include the generation of carbon credits or the development of the land for windparks.

Another benefit of investing in timber and forestry is the potential for diversification. According to research by Nuveen in 2021, private investments in illiquid real assets such as timberland and farmland have demonstrated low or negative correlations with equities and fixed income, providing resilience and diversification from uncorrelated market exposure. One of the reasons for this lack of correlation is the portion of the investment return generated through biological growth, which is independent of market movements. Additionally, payments for ecosystem services such as carbon credits provide another source of uncorrelated returns that have the potential to improve the diversification benefits of timberland investments.

Navigating the risks of forestry funds: what investors need to know

While forestry funds offer the potential for long-term growth and diversification, they also carry significant risks that investors must consider before committing capital.

From an asset perspective, one of the primary risks is the potential for natural disasters, such as wildfires, droughts or storms, to damage or destroy forests. While insurance can provide some protection against these risks, it typically does not cover the full value of the lost timber. Concerns regarding deforestation, illegal logging and land rights disputes have raised questions about the sustainability of some forestry investments. Investors are urged to conduct thorough due diligence and engage with reputable fund managers that adhere to internationally recognized standards, such as the Forest Stewardship Council (FSC) and Programme for the Endorsement of Forest Certification (PEFC).

Another risk of investing in timber and forestry is the potential for changes in government regulations or policies to affect the industry. Similarly, changes in trade policies or tariffs could affect demand for wood products, potentially reducing return on investment. As with any investment, forestry funds carry their own set of risks, including currency risks and costs. The majority of the world's forest-rich countries are located overseas, including Russia, Brazil, Canada, the US and China. This means that investors in forestry funds must be prepared to deal with potential currency fluctuations and foreign transaction fees.

Regarding the funds themselves, one of the most significant disadvantages/risks is illiquidity. Timber investments are still quite an uncommon asset, therefore the market doesn't guarantee a rapid sale – and even pooling investments with others in forestry funds does not necessarily solve this problem. Typical lock-in periods for forestry funds can be 10 years or more, making them illiquid investments that require a long-term investment horizon. In addition to illiquidity, income from forestry investments can be unpredictable. Forestry provides income when the trees are harvested, but when the timber price falls, it is common to delay harvesting, resulting in a halt to that income. Growth can also take years, and investors need to be patient and willing to incur costs while waiting for their trees to grow.

Valuing forestry investments can be challenging, as the timber price is notoriously volatile and data on the industry can be opaque and infrequent. Forestry valuations are therefore complex and require careful consideration of a range of factors, such as soil quality, climate and the maturity of the trees.

The future of forestry funds

Sustainability as we know it today has been defined by forestry. It was first mentioned in the 17th century by Hans Carl von Carlowitz who managed the natural resources of forests in a long-term responsible way by only harvesting the amount of timber that the forest could regrow. Intergenerational management of forests is key in the long-term success of this asset class. After all, we will not be the ones harvesting what we plant today. For long-term investors, who are looking for stable long-term returns paired with low volatility and the benefit of an investment opportunity with a positive environmental impact, forestry is a great addition to any portfolio.

With the Sustainable Finance Disclosure Regulation's (SFDR) stricter implementation since the start of 2023, timing favors the forestry fund sector, providing an opportunity to demonstrate their dedication to responsible forestry practices and Co2 savings. By disclosing their environmental, social, and governance (ESG) characteristics and carbon footprint, forestry funds can distinguish themselves in a crowded investment landscape. As such, forestry fund managers should view the SFDR as a chance to demonstrate their commitment and attract new investors, as sustainability becomes a standard requirement.

The outlook for forestry funds remains optimistic – as the world grapples with the devastating effects of climate change, the need for sustainable and renewable resources will only increase. With their dual benefits of attractive financial returns and positive environmental impacts, forestry funds are well-positioned to become a crucial component of the global investment landscape in the coming years. In a changing market, forestry funds have the potential to move from a niche investment category to a mainstream one.

Summary

In the face of an unpredictable global economy, investors are seeking out resilient and profitable asset classes. Forestry and timber funds are emerging as a sustainable and attractive asset for investors. With the growing awareness around climate change and the rising demand for timber products, this "green goldmine" is proving to be a promising avenue for long-term capital growth. Let's dive deep into the increasing interest in investing in timber and forestry and explore the benefits and risks of this alternative asset class