EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

3) Empower humans

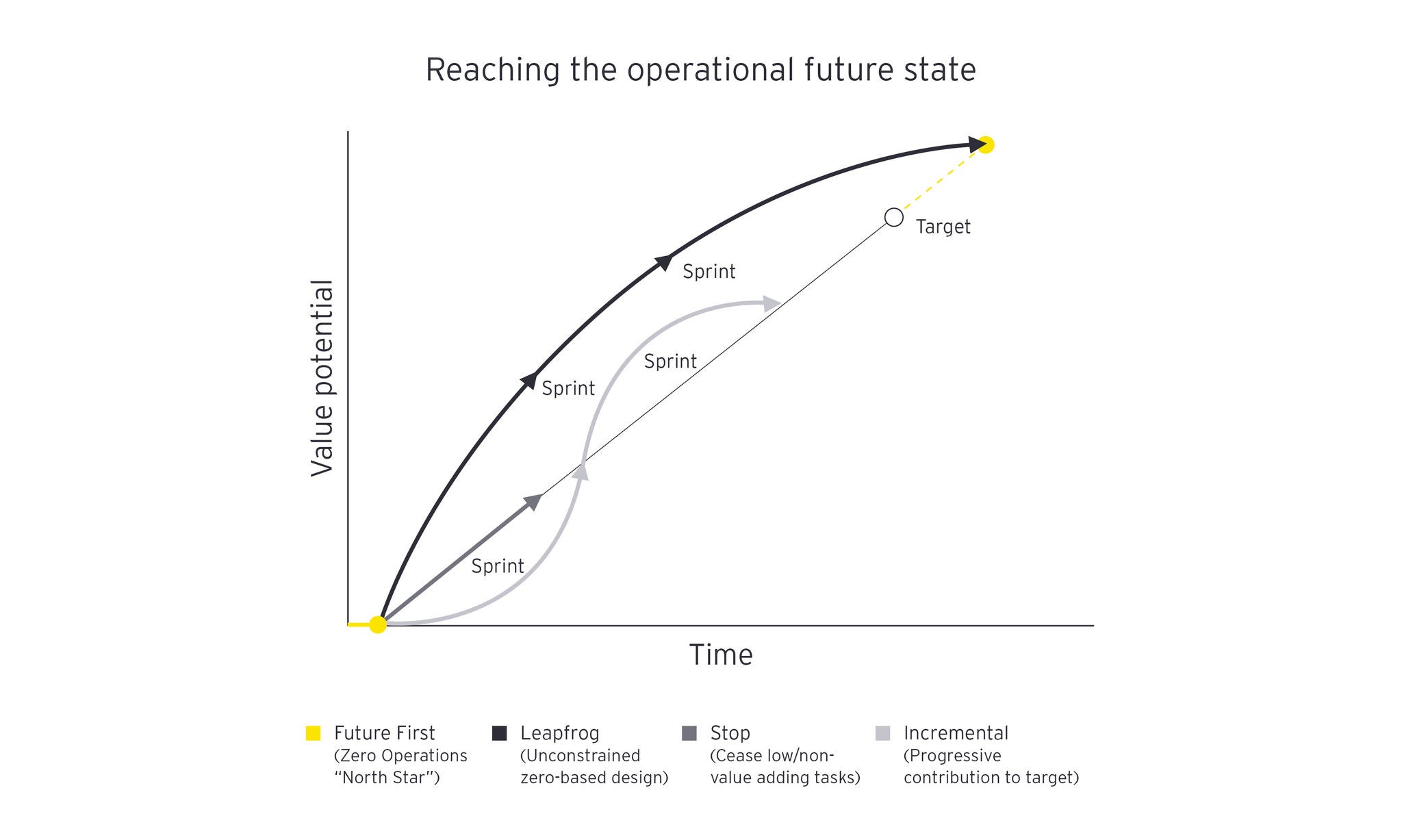

COOs and their teams face significant challenges delivering scale transformation, balancing distinct but highly interrelated priorities such as customer-centricity, cost efficiency and scalability, security, cloud, talent and risk management, and resiliency, all while keeping the lights on in a highly regulated environment.

The cognitive load on the workforce is increasingly demanding. There needs to be a greater focus on the augmentation of employees’ decision-making over time – requiring the execution of a defined decision-intelligence strategy integrated with existing automation and data strategies. Providing employees with recommendations and decision-making context to become more productive and make higher quality decisions more consistently and potentially faster will support the scale and speed of transformation.

Many current perspectives on this emerging topic focus on how technology, such as artificial intelligence (AI) and machine learning (ML), may be applied to augment decision-making, such as for faster and more accurate fraud investigations. This is too narrow a viewpoint to successfully unlock meaningful business value. Decision intelligence is a blend of managerial science, decision theory, social science and data science, necessitating multi-disciplinary teams whose composition will evolve.

Augmenting human effort through decision intelligence is one enabler to humans making greater contributions to ongoing operational transformation and execution of business as usual. More broadly, EY research with Oxford Said Business School found that organizations that put humans at the center of transformations are 2.6 times more likely to succeed than those that don’t. The research also highlights the importance of clearly and frequently articulating banks’ transformation vision and strategy.

4) Setting the sustainability example

Recent EY analysis has found that more than 80 of the world’s 100 largest banks have committed to net zero by 2050. Banks must drive toward these commitments with a zero-carbon vision to guide them in their operations – and with suppliers and ecosystem partners. COOs have a critical role to play, working with sustainability leadership in their organizations and ultimately aligning with the expectations of boards, shareholders, regulators and employers.

Banking COOs and their teams are likely to have accountability for a significant proportion of their organization’s employee base. They will directly influence material drivers of greenhouse gas emissions, such as real estate and business travel. COOs must ensure they recognize that their actions will effectively set the tone for the entire organization’s sustainability drive – and embed a zero-carbon mindset within an overall zero-operations strategy. It’s a significant responsibility.

A zero-operations strategy will likely result in deeper relationships with third parties, such as through greater use of industry utilities and managed services. COOs and their procurement teams will also need to recognize the importance of ensuring those organizations are aligned with the goals of the Paris Agreement and the broader regulatory environment.

EY's Andrew Wickham, Director, Banking Technology, Ernst & Young LLP has contributed to this article.