EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

-

Discover how EY's finance consulting services can help your business capitalize on opportunities to drive profitable growth and drive transformative change.

Read more

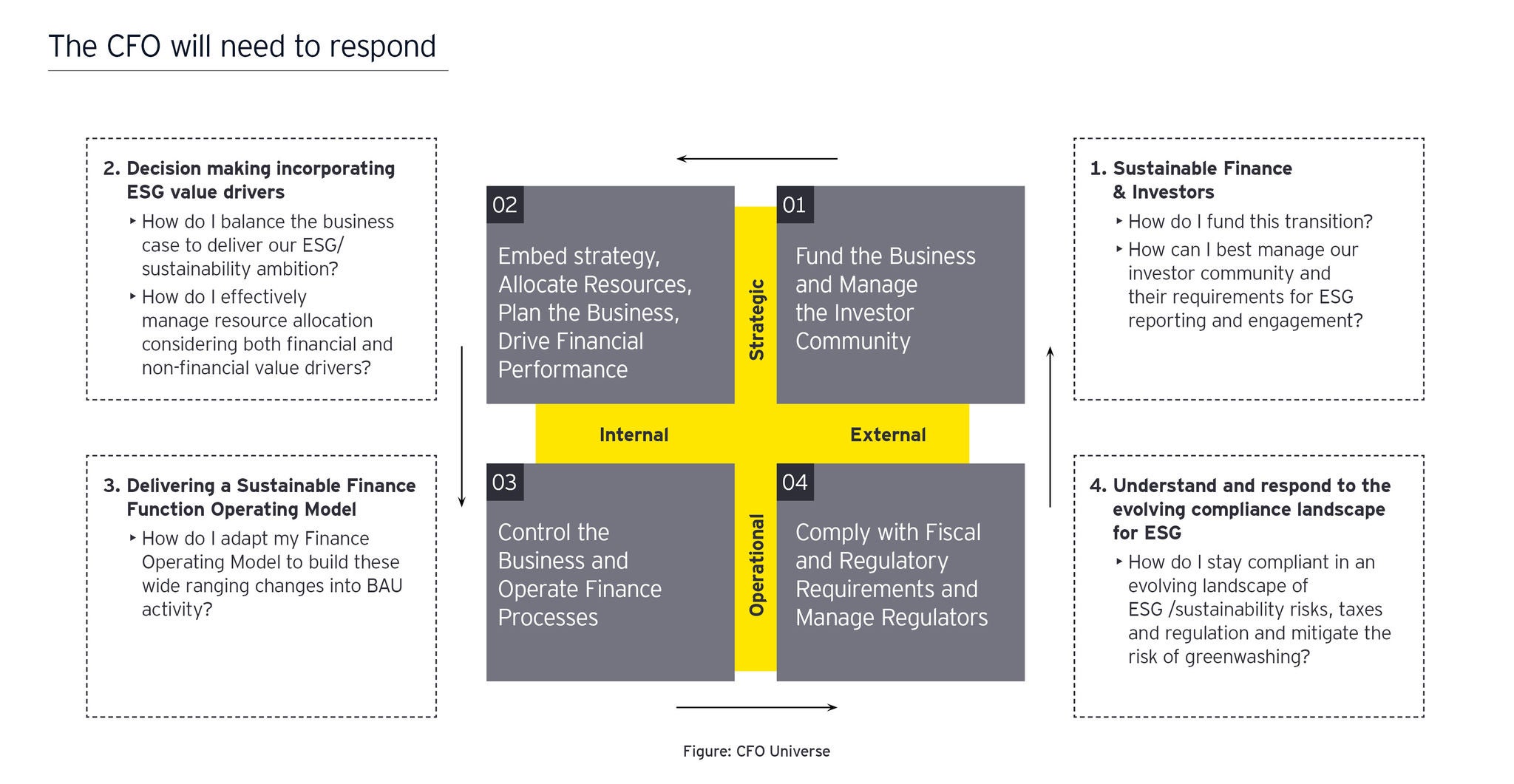

Figure 3: CFO's four dimensions of sustainability

The impact on Danish listed companies

Denmark has a strong tradition of corporate sustainability reporting and has been ranked among the top countries in terms of ESG disclosure quality and quantity.

Despite the high level of quality in sustainability reporting among listed Danish companies, there is still room for improvement in terms of consistency, comparability and relevance. The CSRD offers Danish listed companies a chance to not only improve their reporting practices and align with EU-wide standards and expectations but also to adapt their operations to meet regulatory requirements and seize the opportunity to gain a competitive edge in the market.

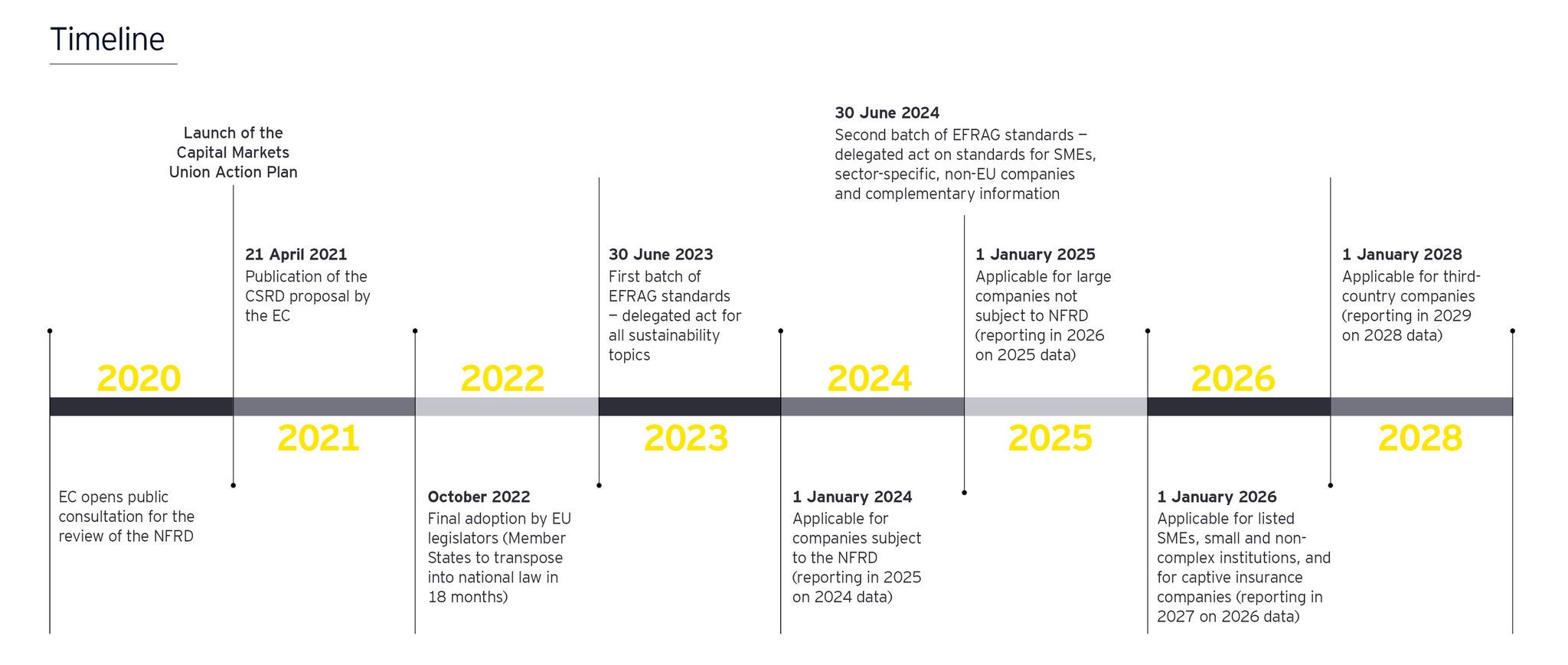

In 2024, companies already reporting under the NFRD will report under CSRD requirements, and in 2025, large companies exceeding the EU’s large company criteria will need to comply with CSRD reporting. As presented in Figure 1, this includes companies that meet at least two of the following criteria:

- Over €20m in total assets

- More than €40m net turnover

- More than 250 employees

This will impact smaller and more growth-oriented companies, such as those listed in First North. It is crucial for companies to start to build their CSRD readiness and embed the data and information requirements in their decision-making process for better visibility in their business operations.

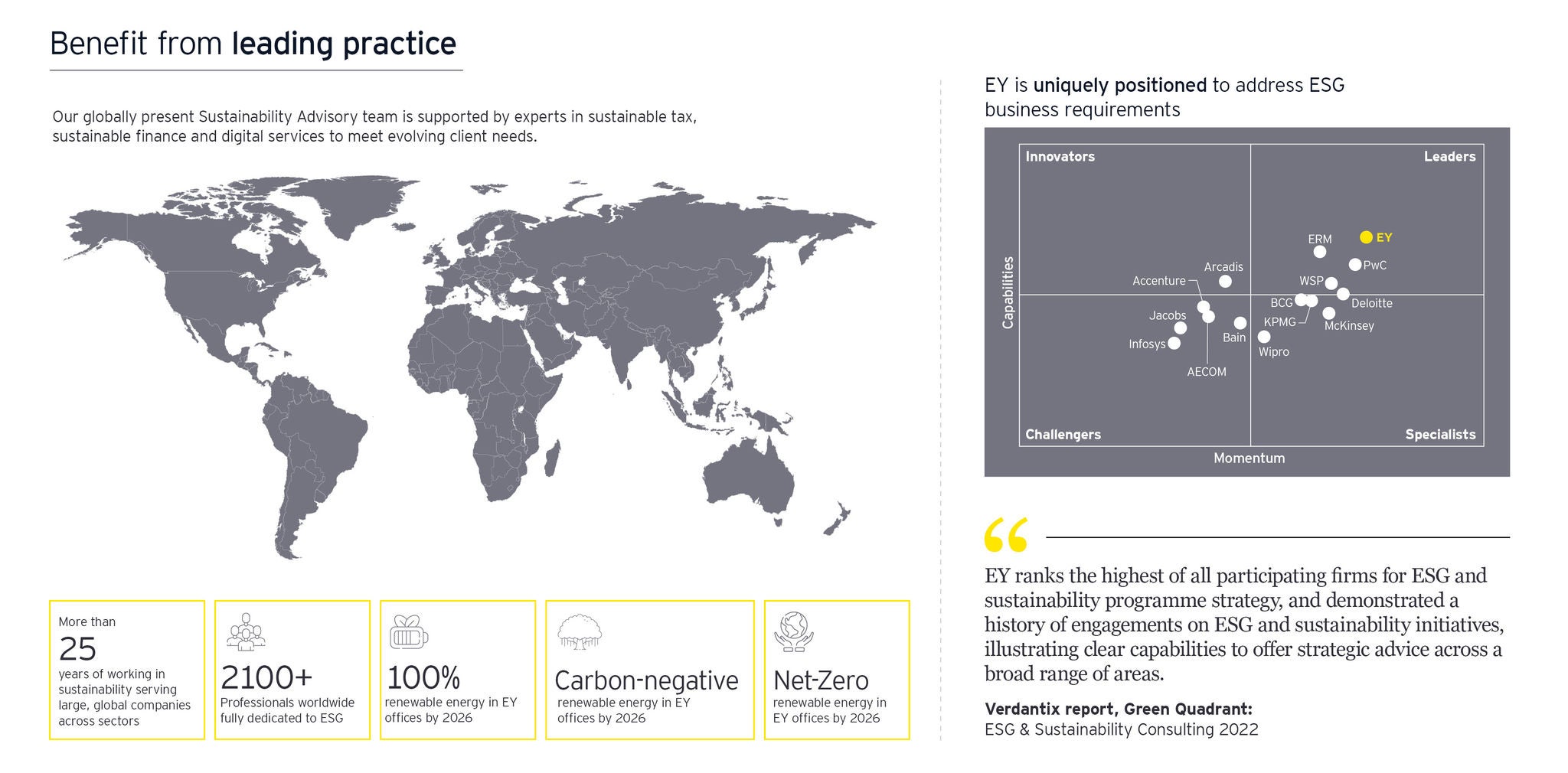

How EY teams can help

As a leading transformation consulting organization in Denmark, has extensive experience and knowledge in helping EY clients with their sustainability reporting needs.

We can help you prepare for the CSRD-led transformation by:

- Conducting a gap analysis of your current reporting practices against CSRD requirements

- Developing a roadmap and action plan for CSRD implementation

- Providing guidance and support on selecting and applying the appropriate reporting framework and standards

- Assisting with data collection, analysis and reporting

- Facilitating the assurance process and help ensuring CSRD compliance

- Communicating your sustainability performance and value creation story to your stakeholders

We can also help you leverage the opportunities that the CSRD offers by:

- Helping you identify and prioritize your material sustainability topics and stakeholders

- Supporting you in setting and monitoring your sustainability goals and targets

- Advising on integrating sustainability into your strategy, governance and risk management

- Supporting you to measure and improve your sustainability impact and outcomes

- Enhancing your sustainability reputation and competitiveness in the EU market

- Embedding CSRD and sustainability in your company’s operating model and daily operations