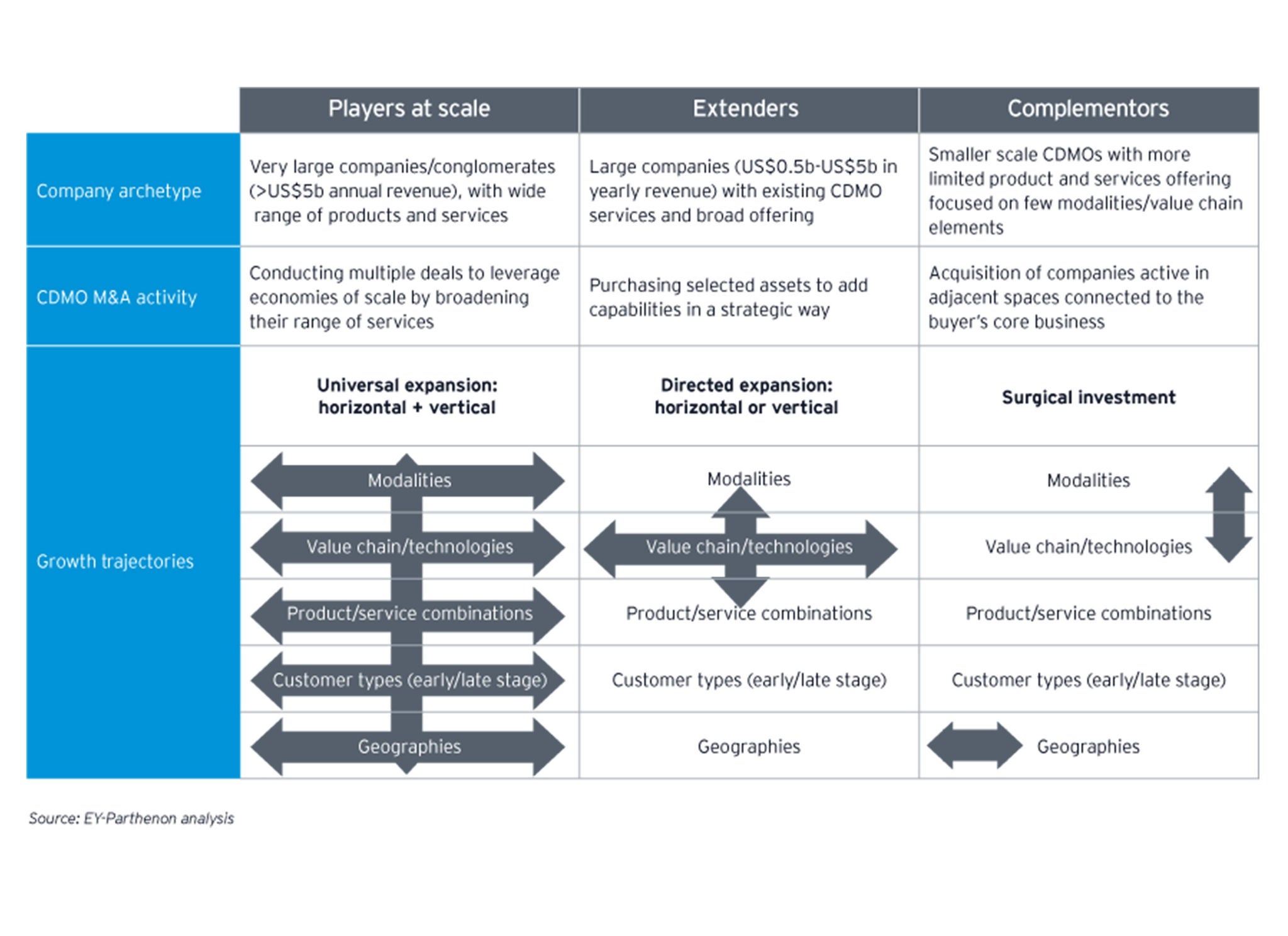

Conclusion and outlook

We see an expansion of the capability of CDMOs is occurring along three main axes:

- The first axis is an expansion of capabilities along value chains within a modality.

- The second axis is an expansion toward new modalities previously not covered.

- The third axis is, in selected cases, an expansion from a focus of product offerings toward offering additional complementing service categories (such as clinical trial services).

Compared to the CDMO M&A activities analyzed in 2012 to 2016,I investment firms appear to have gained appetite to become more active players in the field, and it is likely that this trend will continue. CDMOs offer an option to enter life sciences and pharmaceutical markets by investing in continuous service revenues, while still benefitting from high growth rates in new therapy areas.

In novel modalities, there is likely to be an increasing shift toward capacity expansion by existing players. Key requirements for CDMOs active in this space are: 1) to be able to swiftly allot manufacturing capacity to enable higher speed to market and 2) to secure long-term capacities for assets. Both requirements are also driven by having sufficient reserves in capacity.

CDMOs are likely to further foster their new role as technology innovators. Major companies increasingly incorporate smaller startups and technology leaders. Product-focused companies are likely to continue to move toward the CDMO service market, while CDMOs will increasingly move toward extended product offering. In addition, integration of clinical trial services could be a new trend for CDMOs to enter high value, low volume segments — for example, personalized medicine. However, a respective business model would be quite different from a more traditional volume first business model.

Distilling the findings of the analysis by EY-Parthenon on the CDMO market over the past five years, CDMOs are likely to become strong contributors to innovation in the pharmaceutical industry. Overall, CDMOs will likely remain key partners for pharmaceutical companies and are expected to gain further relevance through their increasing technological expertise and know-how along the value chain.