EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

How EY can help

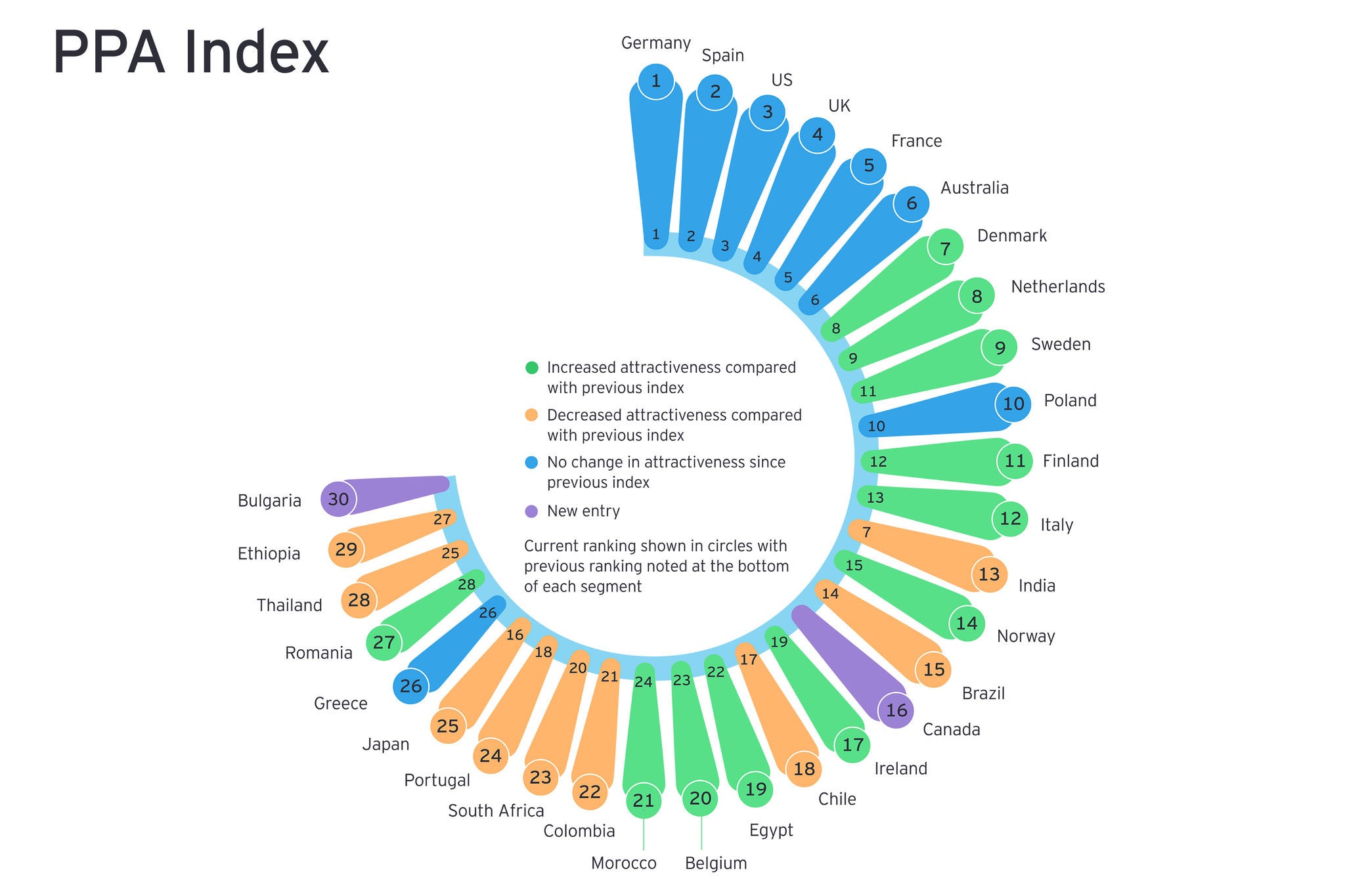

-

Discover how EY's global renewables team can help your business transition to the world of renewable energy.

Read more

The offshore wind sector is at a crucial point in its global development, and change is in the air. Widely viewed as a runaway success over the past 30 years, the sector is now facing its greatest challenge.

Supply chain problems have resulted in global project costs rising by 39% since 2019.2 Schemes in late-stage development are being delayed, or even canceled, by developers that say increased equipment and construction costs mean they can no longer make a return on their investment. Over the next decade, cost inflation could add around US$280b in capital expenditure for the offshore wind sector (excluding China).3

The constant drive to make turbines cheaper and bigger means the supply chain doesn’t have time to recoup the costs of R&D before more is demanded. It pushes up the cost of R&D, labor and vessels, and introduces risk and volatility into the sector. This has been compounded by supply chain imbalances on the back of the COVID-19 pandemic and the war in Ukraine, and created uncertainty with the economics of projects.

This uncertainty has been reflected in recent sustainable energy auctions. The UK’s fifth allocation round in September — using a contract for difference (CfD) model to agree the price to sell electricity — failed to attract a single bidder for offshore wind. The “strike price” set by the UK government was not enough to entice developers to bid.4

Some auctions for US lease areas have also run out of steam. Those off the East Coast attracted record-breaking prices in February 2022, but the more recent Gulf of Mexico auctions attracted very low levels of developer interest.5

The sector is not broken, however. Germany’s first dynamic offshore wind auctions, in July — for the rights to build, using a “buy now pay later” format — attracted bids totaling €12.6b (US$13.46b) for projects in the North Sea and the Baltic Sea. Other markets have also successfully concluded offshore wind tenders at reasonable prices, including Ireland, the Netherlands and Lithuania.

These contrasting auction outcomes reflect the current turbulence in the sector, and it is becoming increasingly clear that factors other than price may need to be considered in the next phase of offshore wind.