EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

Related article

How to optimize your global strategy amid asymmetric globalization

Exploring future scenarios reveals divergent paths for geopolitics, economic policies, sector trajectories and company strategies. Learn more.

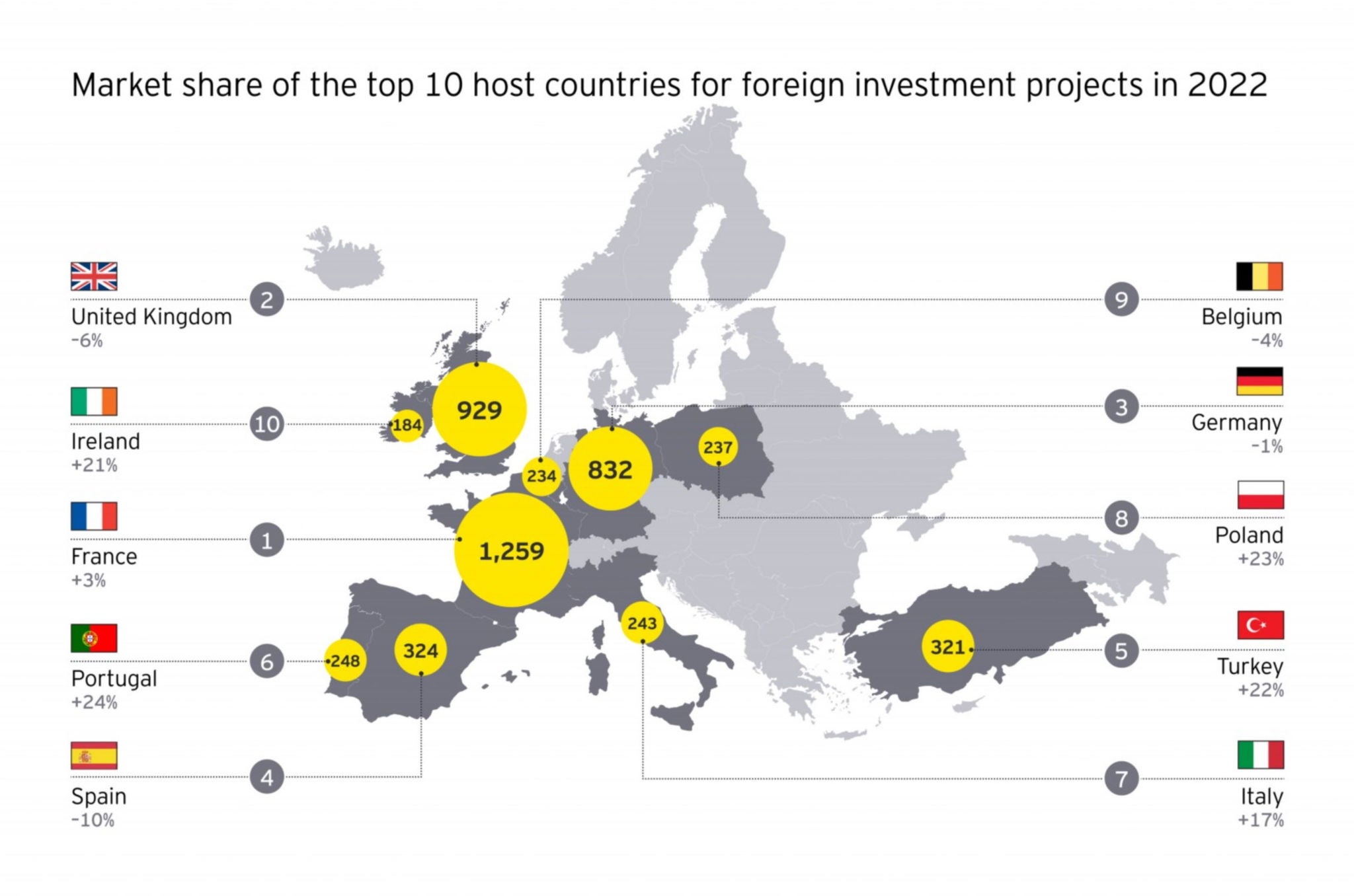

The research suggests businesses think the worst is over. A large number of businesses surveyed — 67% — say they have plans to expand or establish European operations over the coming year, an all-time high and up from 53% a year ago. This reflects two intersecting factors: On the one hand, pent-up demand and the deferred plans of recent years are fueling a new wave of growth and capacity investments; on the other hand, economic conditions require intense reorganization, rationalization and cost optimization activity.

Marc Lhermitte, Partner, EY Consulting, Global Lead – FDI & Attractiveness, says: “If Europe is to capture the pent-up demand and deferred plans, it will be essential to build a compelling business case for global investors in the context of competition from the US and China.”

The US is luring investors with its Inflation Reduction Act (IRA). For EU member states, funding from the EU Resilience and Recovery program could materially change how Europe’s economy evolves. The program is designed to deliver a post-pandemic economic lift via support for digital, renewables and skills development.

“Europe’s critical ambition should be to create the conditions for business to manufacture in Europe, invest in R&D, and make the digital and green investments that will power future prosperity,” says Julie Teigland, EY EMEIA Area Managing Partner. “The time to act is now.”